On my trip to Singapore two weeks ago I read through a new book The Age of Cryptocurrency, written by Michael Casey and Paul Vigna — two journalists with The Wall Street Journal.

Let’s start with the good. I think Chapter 2 is probably the best chapter in the book and the information mid-chapter is some of the best historical look on the topic of previous electronic currency initiatives. I also think their writing style is quite good. Sentences and ideas flow without any sharp disconnects. They also have a number of endnotes in the back for in-depth reading on certain sub-topics.

In this review I look at each chapter and provide some counterpoints to a number of the claims made.

Note: I manually typed the quotes from the book, all transcription errors are my own and should not reflect on the book itself. See my other book reviews.

Introduction

Introduction

The book starts by discussing a company now called bitLanders which pays content creators in bitcoin. The authors introduce us to Francesco Rulli who pays his bloggers in bitcoin and tries to forbid them from cashing out in fiat, so that they create a circular flow of income.1 One blogger they focus on is Parisa Ahmadi, a young Afghani woman who lacks access to the payment channels and platforms that we take for granted. It is a nice feel good story that hits all the high notes.

Unfortunately the experience that individuals like Ahmadi, are not fully reflective of what takes place in practice (and this is not the fault of bitLanders).

For instance, the authors state on p. 2 that:

“Bitcoins are stored in digital bank accounts or “wallets” that can be set up at home by anyone with Internet access. There is no trip to the bank to set up an account, no need for documentation or proof that you’re a man.”

This is untrue in practice. Nearly all venture capital (VC) funded hosted “wallets” and exchanges now require not only Know-Your-Customer (KYC) but in order for any type of fiat conversion, bank accounts. Thus there is a paradox: how can unbanked individuals connect a bank account they do not have to a platform that requires it? This question is never answered in the book yet it represents the single most difficult aspect to the on-boarding experience today.

Starting on page 3, the authors use the term “digital currency” to refer to bitcoins, a practice done throughout the remainder of the book. This contrasts with the term “virtual currency” which they only use 12 times — 11 of which are quotes from regulators. The sole time “virtual currency” is not used by a regulator to describe bitcoins is from David Larimer from Invictus (Bitshares). It is unclear if this was an oversight.

Is there a difference between a “digital currency” and “virtual currency”? Yes. And I have made the same mistake before.

Cryptocurrencies such as bitcoin are not digital currencies. Digital currencies are legal tender, as of this writing, bitcoins are not. This may seem like splitting hairs but the reason regulators use the term “virtual currency” still in 2015 is because no jurisdiction recognizes bitcoins as legal tender.

In contrast, there are already dozens of digital currencies — nearly every dollar that is spent on any given day in the US is electronic and digital and has been for over a decade. This issue also runs into the discussion on nemo dat described a couple weeks ago.

On page 4 the authors very briefly describe the origination of currency exchange which dates back to the Medici family during the Florentine Renaissance. Yet not once in the book is the term “bearer asset” mentioned. Cryptocurrencies such as bitcoin are virtual bearer instruments and as shown in practice, a mega pain to safely secure.

500 years ago bearer assets were also just as difficult to secure and consequently individuals outsourced the security of it to what we now call banks. And this same behavior has once again occurred as large quantities — perhaps the majority — of bitcoins now are stored in trusted third party depositories such as Coinbase and Xapo.

Why is this important?

Again recall that the term “trusted third party” was used 11 times (in the body, 13 times altogether) in the original Nakamoto whitepaper; whoever created Bitcoin was laser focused on building a mechanism to route around trusted third parties due to the additional “mediation and transaction costs” (section 1) these create. Note: that later on page 29 they briefly mentioned legal tender laws and coins (as it related to the Roman Empire).

On page 8 the authors describe the current world as “tyranny of centralized trust” and on page 10 that “Bitcoin promises to take at least some of that power away from governments and hand it to the people.”

While that may be a popular narrative on social media, not everyone involved with Bitcoin (or the umbrella “blockchain” world) holds the same view. Nor do the authors describe some kind of blue print for how this is done. Recall that in order to obtain bitcoins in the first place a user can do one of three things:

- mine bitcoins

- purchase bitcoins from some kind of exchange

- receive them for payments (e.g., merchant activity)

In practice mining is out of the hands of “the people” due to economies of scale which have trended towards warehouse mining – it is unlikely that embedded ASICs such as from 21 inc, will change that dynamic much, if any. Why? Because for every device added to the network a corresponding amount of difficulty is also added, diluting the revenue to below dust levels.

Remember how Tom Sawyer convinced kids to whitewash a fence and they did so eagerly without question? What if he asked you to mine bitcoins for him for free? A trojan botnet? While none of the products have been announced and changes could occur, from the press release that seems to be the underlying assumption of the 21.co business model.

In terms of the second point, nearly all VC funded exchanges require KYC and bank accounts. The ironic aspect is that “unbanked” and “underbanked” individuals often lack the necessary “valid” credentials that can be used by cheaper automated KYC technology (from Jumio) and thus expensive manual processing is done, costs that must be borne by someone. These same credential-less individuals typically lack a bank account (hence the name “unbanked”).

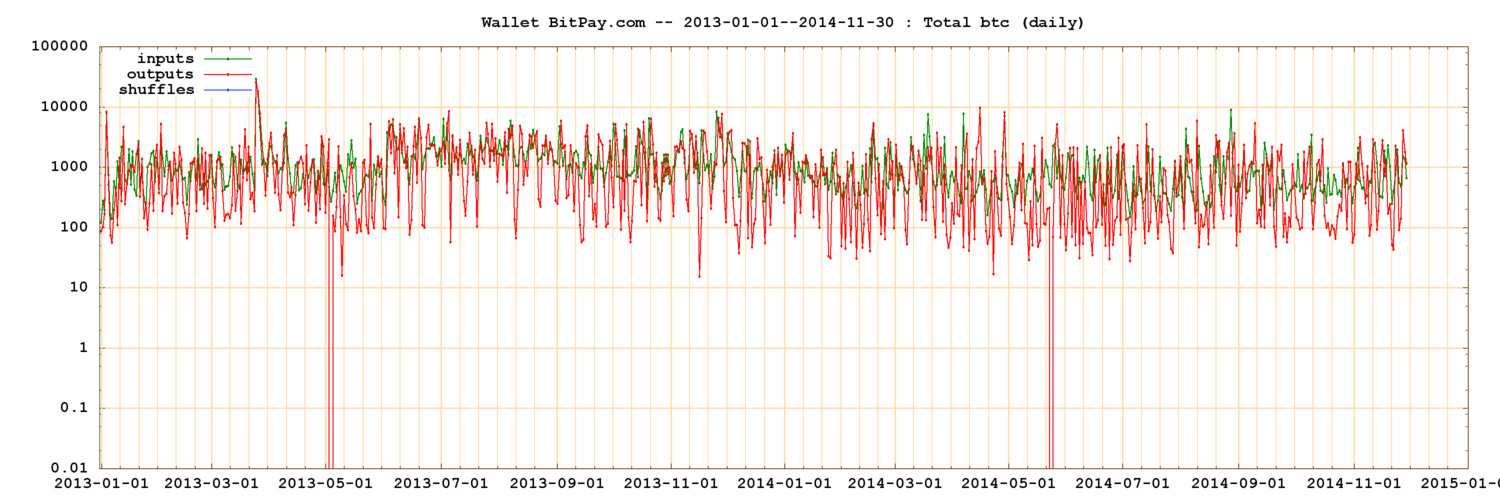

Lastly with the third point, while there are any number of merchants that now accept bitcoin, in practice very few actually do receive bitcoins on any given day. Several weeks ago I broke down the numbers that BitPay reported and the verdict is payment processing is stagnant for now.

Why is this last point important to what the authors refer to as “the people”?

Ten days after Ripple Labs was fined by FinCEN for not appropriately enforcing AML/KYC regulations, Xapo — a VC funded hosted wallet startup — moved off-shore, uprooting itself from Palo Alto to Switzerland. While the stated reason is “privacy” concerns, it is likely due to regulatory concerns of a different nature.

In his interview with CoinDesk last week, Wences Casares, the CEO and founder of Xapo noted that:

Still, Casares indicated that Xapo’s customers are most often using its accounts primarily for storage and security. He noted that many of its clientele have “never made a bitcoin payment”, meaning its holdings are primarily long-term bets of high net-worth customers and family offices.

“Ninety-six percent of the coins that we hold in custody are in the hands of people who are keeping those coins as an investment,” Casares continued.

96% of the coins held in custody by Xapo are inert. According to a dated presentation, the same phenomenon takes place with Coinbase users too.

Perhaps this behavior will change in the future, though, if not it seems unclear how this particular “to the people” narrative can take place when few large holders of a static money supply are willing to part with their virtual collectibles. But this dovetails into differences of opinion on rebasing money supplies and that is a topic for a different post.

On page 11 the authors describe five stages of psychologically accepting Bitcoin. In stage one they note that:

Stage One: Disdain. Not even denial, but disdain. Here’s this thing, it’s supposed to be money, but it doesn’t have any of the characteristics of money with which we’re familiar.

I think this is unnecessarily biased. While I cannot speak for other “skeptics,” I actually started out very enthusiastic — I even mined for over a year — and never went through this strange five step process. Replace the word “Bitcoin” with any particular exciting technology or philosophy from the past 200 years and the five stage process seems half-baked at best.

On page 13 they state:

“Public anxiety over such risks could prompt an excessive response from regulators, strangling the project in its infancy.”

Similarly on page 118 regarding the proposed New York BitLicense:

“It seemed farm more draconian than expected and prompted an immediate backlash from a suddenly well-organized bitcoin community.”

This is a fairly alarmist statement. It could be argued that due to its anarchic code-as-law coupled with its intended decentralized topology, that it could not be strangled. If a certain amount of block creating processors (miners) was co-opted by organizations like a government, then a fork would likely occur and participants with differing politics would likely diverge.

A KYC chain versus an anarchic chain (which is what we see in practice with altchains such as Monero and Dash). Similarly, since there are no real self-regulating organizations (SRO) or efforts to expunge the numerous bad actors in the ecosystem, what did the enthusiasts and authors expect would occur when regulators are faced with complaints?

With that said — and I am likely in a small minority here — I do not think the responses thus far from US regulators (among many others) has been anywhere near “excessive,” but that’s my subjective view. Excessive to me would be explicitly outlawing usage, ownership and mining of cryptocurrencies. Instead what has occurred is numerous fact finding missions, hearings and even appearances by regulators at events.

On page 13 the authors state that:

“Cryptocurrency’s rapid development is in some ways a quirk of history: launched in the throes of the 2008 financial crisis, bitcoin offered an alternative to a system — the existing financial system — that was blowing itself up and threatening to take a few billion people down with it.”

This is retcon. Satoshi Nakamoto, if he is to be believed, stated that he began coding the project in mid-2007. It is more of a coincidence than anything else that this project was completed around the same time that global stock indices were at their lowest in decades.

Chapter 1

On page 21 the authors state that:

“Bitcoin seeks to address this challenge by offering users a system of trust based not on human being but on the inviolable laws of mathematics.”

While the first part is true, it is a bit cliche to throw in the “maths” reason. There are numerous projects in the financial world alone that are run by programs that use math. In fact, all computer programs and networks use some type of math at their foundation, yet no one claims that the NYSE, pace-makers, traffic intersections or airplanes are run by “math-based logic” (or on page 66, “”inviolable-algorithm-based system”).

A more accurate description is that Bitcoin’s monetary system is rule-based, using a static perfectly inelastic supply in contrast to either the dynamic or discretionary world humans live in. Whether this is desirable or not is a different topic.

On page 26 they describe the Chartalist school of thought, the view that money is political, that:

“looks past the thing of currency and focuses instead on the credit and trust relationships between the individual and society at large that currency embodies” […] “currency is merely the token or symbol around which this complex system is arranged.”

This is in contrast to the ‘metallist’ mindset of some others in the Bitcoin community, such as Wences Casares and Jon Matonis (perhaps there is a distinct third group for “barterists”?).

I thought this section was well-written and balanced (e.g., appropriate citation of David Graeber on page 28; and description of what “seigniorage” is on page 30 and again on page 133).

On page 27 the authors write:

Yet many other cryptocurrency believers, including a cross section of techies and businessmen who see a chance to disrupt the bank centric payments system are de facto charatalists. They describe bitcoin not as a currency but as a payments protocol.

Perhaps this is true. Yet from the original Nakamoto whitepaper, perhaps he too was a chartalist?

Stating in section 1:

Commerce on the Internet has come to rely almost exclusively on financial institutions serving as trusted third parties to process electronic payments. While the system works well enough for most transactions, it still suffers from the inherent weaknesses of the trust based model. Completely non-reversible transactions are not really possible, since financial institutions cannot avoid mediating disputes. The cost of mediation increases transaction costs, limiting the minimum practical transaction size and cutting off the possibility for small casual transactions, and there is a broader cost in the loss of ability to make non-reversible payments for non-reversible services. With the possibility of reversal, the need for trust spreads. Merchants must be wary of their customers, hassling them for more information than they would otherwise need. A certain percentage of fraud is accepted as unavoidable. These costs and payment uncertainties can be avoided in person by using physical currency, but no mechanism exists to make payments over a communications channel without a trusted party.

A payments rail, a currency, perhaps both?

Fun fact: the word “payment” appears 12 times in the whole white paper, just one time less than the word “trust” appears.

On page 29 they cite the Code of Hammurabi. I too think this is a good reference, having made a similar reference to the Code in Chapter 2 of my book last year.

On page 31 they write:

“Today, China grapples with competition to its sovereign currency, the yuan, due both to its citizens’ demand for foreign national currencies such as the dollar and to a fledgling but potentially important threat from private, digital currencies such as bitcoin.”

That is a bit of a stretch. While Chinese policy makers do likely sweat over the creative ways residents breach and maneuver around capital controls, it is highly unlikely that bitcoin is even on the radar as a high level “threat.” There is no bitcoin merchant economy in China.

The vast majority of activity continues to be related to mining and trading on exchanges, most of which is inflated by internal market making bots (e.g., the top three exchanges each run bots that dramatically inflate the volume via tape painting). And due to how WeChat and other social media apps in China frictionlessly connect residents with their mainland bank accounts, it is unlikely that bitcoin will make inroads in the near future.

On page 36 they write:

“By 1973, once every country had taken its currency off the dollar peg, the pact was dead, a radical change.”

In point of fact, there are 23 countries that still peg their currency to the US dollar. Post-1973 saw a number of flexible and managed exchange rate regimes as well as notable events such as the Plaza Accord and Asian Financial Crisis (that impacted the local pegs).

On page 39 they write:

“By that score, bitcoin has something to offer: a remarkable capacity to facilitate low-cost, near-instant transfer of value anywhere in the world.”

The point of contention here is the “low-cost” — something that the authors never really discuss the logistics of. They are aware of “seigniorage” and inflationary “block rewards” yet they do not describe the actual costs of maintaining the network which in the long run, the marginal costs equal the marginal value (MC=MV).

This is an issue that I tried to bring up with them at the Google Author Talk last month (I asked them both questions during the Q&A):

The problem for Vigna’s view, (starting around 59m) is that if the value of a bitcoin fell to $30, not only would the network collectively “be cheaper” to maintain, but also to attack.

On paper, the cost to successfully attack the network today by obtaining more than 50% of the hashrate at this $30 price point would be $2,250 per hour (roughly 0.5 x MC) or roughly an order of magnitude less than it does at today’s market price (although in practice it is a lot less due to centralization).

Recall that the security of bitcoin was purposefully designed around proportionalism, that in the long run it costs a bitcoin to secure a bitcoin. We will talk about fees later at the end of next chapter.

Chapter 2

On page 43, in the note at the bottom related to Ray Dillinger’s characterization that bitcoin is “highly inflationary” — Dillinger is correct in the short run. The money supply will increase by 11% alone this year. And while in the long run the network is deflationary (via block reward halving), the fact that the credentials to the bearer assets (bitcoins) are lost and destroyed each year results in a non-negligible amount of deflation.

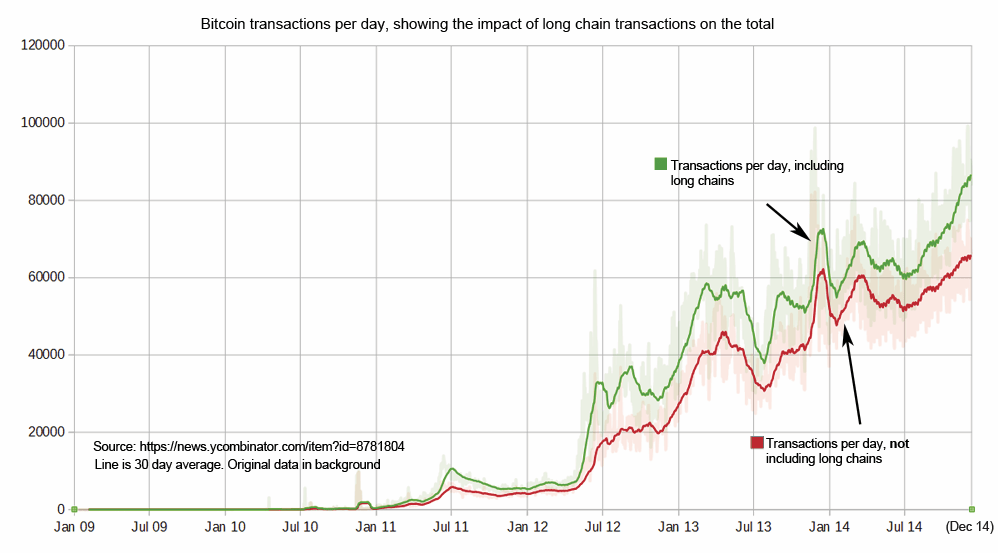

For instance, in chapter 12 I noted some research: in terms of losing bitcoins, the chart below illustrates what the money supply looks like with an annual loss of 5% (blue), 1% (red) and 0.1% (green) of all mined bitcoins.

Source: Kay Hamacher and Stefan Katzenbeisser

In December 2011, German researchers Kay Hamacher and Stefan Katzenbeisser presented research about the impact of losing the private key to a bitcoin. The chart above shows the asymptote of the money supply (Y-axis) over time (X-axis).

According to Hamacher:

So to get rid of inflation, they designed the protocol that over time, there is this creation of new bitcoins – that this goes up and saturates at some level which is 21 million bitcoins in the end.

But that is rather a naïve picture. Probably you have as bad luck I have, I have had several hard drive crashes in my lifetime, and what happens when your wallet where your bitcoins are stored and your private key vanish? Then your bitcoins are probably still in the system so to speak, so they are somewhat identifiable in all the transactions but they are not accessible so they are of no economic value anymore. You cannot exchange them because you cannot access them. Or think more in the future, someone dies but his family doesn’t know the password – no economic value in those bitcoins anymore. They cannot be used for any exchange anymore. And that is the amount of bitcoins when just a fraction per year vanish for different fractions. So the blue curve is 5% of all the bitcoins per year vanish by whatever means there could be other mechanisms.

It is unclear exactly how many bitcoins can be categorized in such a manner today or what the decay rate is.

On page 45 the authors write:

Some immediately homed in on a criticism of bitcoin that would become common: the energy it would take to harvest “bitbux” would cost more than they were worth, not to mention be environmentally disastrous.

While I am unaware of anyone who states that it would cost more than what they’re worth, as stated in Appendix B and in Chapter 3 (among many other places), the network was intentionally designed to be expensive, otherwise it would be “cheap to attack.” And those costs scale in proportion to the token value.

As noted a few weeks ago:

For instance, last year O’Dwyer and Malone found that Bitcoin mining consumes roughly the same amount of energy as Ireland does annually. It is likely that their estimate was too high and based on Dave Hudson’s calculations closer to 10% of Ireland’s energy consumption.23 Furthermore, it has likely declined since their study because, as previously explored in Appendix B, this scales in proportion with the value of the token which has declined over the past year.

The previous post looked at bitcoin payments processed by BitPay and found that as an aggregate the above-board activity on the Bitcoin network was likely around $350 million a year. Ireland’s nominal GDP is expected to reach around $252 billion this year. Thus, once Hudson’s estimates are integrated into it, above-board commercial bitcoin activity appears to be about two orders of magnitude less than what Ireland produces for the same amount of energy.

Or in other words, the original responses to Nakamoto six and a half years ago empirically was correct. It is expensive and resource intensive to maintain and it was designed to be so, otherwise it would be easy to attack, censor and modify the history of votes.

Starting on page 56 they describe Mondex, Secure Electronic Transaction (SET), Electronic Monetary System, Citi’s e-cash model and a variety of other digital dollar systems that were developed during the 1990s. Very interesting from a historical perspective and it would be curious to know what more of these developers now think of cryptocurrency systems. My own view, is that the middle half of Chapter 2 is the best part of the book: very well researched and well distilled.

On page 64 they write:

[T]hat Nakamoto launched his project with a reminder that his new currency would require no government, no banks and no financial intermediaries, “no trusted third party.”

In theory this may be true, but in practice, the Bitcoin network does not natively provide any of the services banks do beyond a lock box. There is a difference between money and the cornucopia of financial instruments that now exist and are natively unavailable to Bitcoin users without the use of intermediaries (such as lending).

On page 66 they write:

He knew that the ever-thinning supply of bitcoins would eventually require an alternative carrot to keep miners engaged, so he incorporated a system of modest transaction fees to compensate them for the resources they contributed. These fees would kick in as time went on and as the payoff for miners decreased.

That’s the theory and the popular narrative.

However, what does it look like in practice?

Source: Blockchain.info

Above is a chart visualizing fees to miners denominated in USD from January 2009 to May 17, 2015. Perhaps the fees will indeed increase to replace block rewards, or conversely, maybe as VC funding declines in the coming years, the companies that are willing and able to pay fees for each transaction declines.

On page 67, the authors introduce us to Laszlo Hanyecz, a computer programmer in Florida who according to the brief history of Bitcoin lore, purchased two Papa John’s pizzas for 10,000 bitcoins on May 22, 2010 (almost five years ago to the day).

He is said to have sold 40,000 bitcoins in this manner and generated all of the bitcoins through mining. He claims to be the first person to do GPU mining, ramping up to “over 800 times” of a CPU; and during this time “he was getting about half of all the bitcoins mined.” According to him, he originally used a Nvidia 9800 GTX+ and later switched to 2 AMD Radeon 5970s. It is unclear how long he mined or when he stopped.

In looking at the index of his server, there are indeed relevant OpenCL software files. If this is true, then he beat ArtForz to GPU mining by at least two months.

Source: Laszlo Hanyecz personal server

On page 77 they write:

Anybody can go on the Web, download the code for no cost, and start running it as a miner.

While technically this is true, that you can indeed download the Satoshi Bitcoin core client for free, restated in 2015 it is not viable for hoi polloi. In practice you will not generate any bitcoins solo-mining on a desktop machine unless you do pooled mining circa 2011.

Today, even pooled mining with the best Xeon processors will be unprofitable. Instead, the only way to generate enough funds to cover both the capital expenditures and operating expenditures is through the purchase of single-use hardware known as an ASIC miner, which is a depreciating capital good.

Mining has been beyond the breakeven reach of most non-savvy home users for two years now, not to mention those who live in developing countries with poor electrical infrastructure or uncompetitive energy rates. It is unlikely that embedded mining devices will change that equation due to the fact that every additional device increases the difficultly level whilst the device hashrate remains static.

This ties in with what the authors also wrote on page 77:

You don’t buy bitcoin’s software as you would other products, which means you’re not just a customer. What’s more, there’s no owner of the software — unlike, say, PayPal, which is part of eBay.

This is a bit misleading. In order to use the Bitcoin network, users must obtain bitcoins somehow. And in practice that usually occurs through trusted third parties such as Coinbase or Xapo which need to identify you via KYC/AML processes.

So while in 2009 their quote could have been true, in practice today that is largely untrue for most new participants — someone probably owns the software and your personal data. In fact, a germane quote on reddit last week stated, “Why don’t you try using Bitcoin instead of Coinbase.”

Furthermore, the lack of “ownership” of Bitcoin is dual-edged as there are a number of public goods problems with maintaining development that will be discussed later.

On page 87 they describe Blockchain.info as a “high-profile wallet and analytics firm.”

I will come back to “wallets” later. Note: most of these “wallets” are likely throwaway, temp wallets used to move funds to obfuscate provenance through the use of Shared Coin (one of the ways Blockchain.info generates revenue is by operating a mixer).

Overall Chapter 3 was also fairly informative. The one additional quibble I have is that Austin and Beccy Craig (the story at the end) were really only able to travel the globe and live off bitcoins for 101 days because they had a big cushion: they had held a fundraiser that raised $72,995 of additional capital. That is enough money to feed and house a family in a big city for a whole year, let alone go globe trotting for a few months.

Chapter 4

On page 99 they describe seven different entities that have access to credit card information when you pay for a coffee at Starbucks manually. Yet they do not describe the various entities that end up with the personal information when signing up for services such as Coinbase, ChangeTip, Circle and Xapo or what these depository institutions ultimately do with the data (see also Richard Brown’s description of the payment card system).

When describing cash back rewards that card issuers provide to customers, on page 100 they write:

Still it’s an illusion to think you are not paying for any of this. The costs are folded into various bank charges: card issuance fees, ATM fees, checking fees, and, of course, the interest charged on the millions of customers who don’t pay their balances in full each month.

Again, to be even handed they should also point out all the fees that Coinbase charges, Bitcoin ATMs charge and so forth. Do any of these companies provide interest-bearing accounts or cash-back rewards?

On page 100 they also stated that:

Add in the cost of fraud, and you can see how this “sand in the cogs” of the global payment system represents a hindrance to growth, efficiency, and progress.

That seems a bit biased here. And my statement is not defending incumbents: global payment systems are decentralized yet many provide fraud protection and insurance — the very same services that Bitcoin companies are now trying to provide (such as FDIC insurance on fiat deposits) which are also not free.

On page 100 they also write:

We need these middlemen because the world economy still depends on a system in which it is impossible to digitally send money from one person to another without turning to an independent third party to verify the identity of the customer and confirm his or her right to call on the funds in the account.

Again, in practice, this is now true for Bitcoin too because of how most adoption continues to take place on the edges in trusted third parties such as Coinbase and Circle.

On page 101 they write:

In letting the existing system develop, we’ve allowed Visa and MasterCard to form a de facto duopoly, which gives them and their banking partners power to manipulate the market, says Gil Luria, an analyst covering payment systems at Wedbush Securities. Those card-network firms “not only get to extract very significant fees for themselves but have also created a marketplace in which banks can charge their own excessive fees,” he says.

Why is it wrong to charge fees for a service? What is excessive? I am certainly not defending incumbents or regulatory favoritism but it is unclear how Bitcoin institutions in practice — not theory — actually are any different.

And, the cost per transaction for Bitcoin is actually quite high (see chart below) relative to these other systems due to the fact that Bitcoin also tries to be a seigniorage system, something that neither Visa or MasterCard do.

Source: Markos05

On page 102 when talking about MasterCard they state:

But as we’ve seen, that cumbersome system, as it is currently designed, is tightly interwoven into the traditional banking system, which always demands a cut.

The whole page actually is a series of apples-and-oranges comparisons. Aside from settlement, the Bitcoin network does not provide any of the services that they are comparing it to. There is nothing in the current network that provides credit/lending services whereas the existing “cumbersome” system was not intentionally designed to be cumbersome, but rather is intertwined and evolved over decades so that customers can have access to a variety of otherwise siloed services.

Again, this is not to say the situation cannot be improved but as it currently exists, Bitcoin does not provide a solution to this “cumbersome” system because it doesn’t provide similar services.

On page 102 and 103 they write about payment processors such as BitPay and Coinbase:

These firms touted a new model to break the paradigm of merchants’ dependence on the bank-centric payment system described above. These services charged monthly fees that amounted to significantly lower transaction costs for merchants than those charged in credit-card transactions and delivered swift, efficient payments online or on-site.

Except this is not really true. The only reason that both BitPay and Coinbase are charging less than other payment processors is that VC funding is subsidizing it. These companies still have to pay for customer service support and fraud protection because customer behavior in aggregate is the same. And as we have seen with BitPay numbers, it is likely that BitPay’s business model is a losing proposition and unsustainable.

On page 103 they mention some adoption metrics:

The good news is found in the steady expansion in the adoption of digital wallets, the software needed to send and receive bitcoins, with Blockchain and Coinbase, the two biggest providers of those, on track to top 2 million unique users each at the time of the writing.

This is at least the third time they talk about wallets this way and is important because it is misleading, I will discuss in-depth later.

Continuing they write that:

Blockchain cofounder Peter Smith says that a surprisingly large majority of its accounts — “many more than you would think,” he says cryptically — are characterized as “active.”

This is just untrue and should have been pressed by the authors. Spokesman from Blockchain.info continue to publish highly inflated numbers. For instance in late February 2015, Blockchain.info claimed that “over $270 million in bitcoin transactions occurred via its wallets over the past seven days.”

This is factually untrue. As I mentioned three months ago:

Organ of Corti pointed out that the 7 day average was indeed ~720,000 bitcoins in total output volume (thus making) the weekly volume would be about “5e06 btc for the network.”

Is it valid to multiply the total output volume by USD (or euros or yen)? No.

Why not? Because most of this activity is probably a combination of wallet shuffling, laundering and mixing of coins (e.g., use of SharedSend and burner wallets) or any number of superfluous activity. It was not $270 million of economic trade.

Blockchain.info’s press release seems to be implying that economic trade is taking place, in which all transactions are (probably) transactions to new individuals when in reality it could simply be a lot of “change” address movement. And more to the point, the actual internal volume looks roughly the same as has been the past few months (why issue a press release now?).

Continuing on page 103 they write:

“For the first eight months months of 2014, around $50 million per day was passing thought the bitcoin network (some of which was just “change” that bitcoin transactions create as an accounting measure)…”

There is a small typo above (in bold) but the important part is the estimate of volume. There is no public research showing a detailed break down of average volume of economic activity. Based on a working paper I published four months ago, it is fairly clear that this figure is probably in the low millions USD at most. Perhaps this will change in the future.

On page 106 they write about Circle and Xapo:

For now, these firms make no charge to cover costs of insurance and security, betting that enough customers will be drawn to them and pay fees elsewhere — for buying and selling bitcoins, for example — or that their growing popularity will allow them to develop profitable merchant-payment services as well. But over all, these undertaking must add costs back into the bitcoin economy, not to mention a certain dependence on “trusted third parties.” It’s one of many areas of bitcoin development — another is regulation — where some businessmen are advocating a pragmatic approach to bolstering public confidence, one that would necessitate compromises on some of the philosophical principles behind a model of decentralization. Naturally, this doesn’t sit well with bitcoin purists.

While Paul Vigna may not have written this, he did say something very similar at the Google Author Talk event (above in the video).

The problem with this view is that it is a red herring: this has nothing to do with purism or non-purism.

The problem is that Bitcoin’s designer attempted to create a ‘permissionless’ system to accommodate pseudonymous actors. The entire cost structure and threat model are tied to this. If actors are no longer pseudonymous, then there is no need to have this cost structure, or to use proof-of-work at all. In fact, I would argue that if KYC/KYM (Know Your Miner) are required then a user might just as well use a database or permissioned system. And that is okay, there are businesses that will be built around that.

This again has nothing to do with purism and everything to do with the costs of creating a reliable record of truth on a public network involving unknown, untrusted actors. If any of those variables changes — such as adding real-world identity, then from a cost perspective it makes little sense to continue using the modified network due to the intentionally expensive proof-of-work.

On page 107 they talk about bitcoin price volatility discussing the movements of gasoline. The problem with this analogy is that no one is trying to use gasoline as money. In practice consumers prefer purchasing power stability and there is no mechanism within the Bitcoin network that can provide this.

For instance:

The three slides above are from a recent presentation from Robert Sams. Sams previously wrote a short paper on “Seigniorage Shares” — an endogenous way to rebase for purchasing power stability within a cryptocurrency.

The three slides above are from a recent presentation from Robert Sams. Sams previously wrote a short paper on “Seigniorage Shares” — an endogenous way to rebase for purchasing power stability within a cryptocurrency.

Bitcoin’s money supply is perfectly inelastic therefore the only way to reflect changes in demand is through changes in price. And anytime there are future expectations of increased or decreased utility, this is reflected in prices via volatility.

Oddly however, on page 110, they write:

A case can be made that bitcoin’s volatility is unavoidable for the time being.

Yet they do not provide any evidence — aside from feel good “Honey Badger” statements — for how bitcoin will somehow stabilize. This is something the journalists should have drilled down on, talking to commodity traders or some experts on fuel hedging strategies (which is something airline companies spend a great deal of time and resources with).

Instead they cite Bobby Lee, CEO of BTC China and Gil Luria once again. Lee states that “Once its prices has risen far enough and bitcoin has proven itself as a store of value, then people will start to use it as a currency.”

This is a collective action problem. Because all participants each have different time preferences and horizons — and are decentralized — this type of activity is actually impossible to coordinate, just ask Josh Garza and the $20 Paycoin floor. This also reminds me of one of my favorite comments on reddit: “Bitcoin will stabilize in price then go to the moon.”

The writers then note that, “Gil Luria, the Wedbush analyst, even argues that volatility is a good thing, on the grounds that it draws profit-seeking traders into the marketplace.”

But just because you have profit-seeking traders in the market place does not mean volatility disappears.

Credit: George Samman

For instance, in the chart above we can see how bitcoin trades relative to commodities over the past year:

- Yellow is DBC

- Red is OIL

- Bars are DXY which is a dollar index

- And candlesticks are BTCUSD

- Brent Crude Futr May12 N/A 13.83

- Gasoline Rbob Fut Dec12 N/A 13.71

- Wti Crude Future Jul12 N/A 13.56

- Heating Oil Futr Jun12 N/A 13.20

- Gold 100 Oz Futr Dec 12 N/A 7.49

- Sugar #11(World) Jul12 N/A 5.50

- Corn Future Dec12 N/A 5.01

- Lme Copper Future Mar13 N/A 4.55

- Soybean Future Nov12 N/A 4.38

- Lme Zinc Future Jul12

It bears mentioning that Ferdinando Ametrano has also described this issue in depth most recently in a presentation starting on slide 15.

Continuing on page 111, the writers note that:

Over time, the expansion of these desks, and the development of more and more sophisticated trading tools, delivered so much liquidity that exchange rates became relatively stable. Luria is imagining a similar trajectory for bitcoin. He says bitcoiners should be “embracing volatility,” since it will help “create the payment network infrastructure and monetary base” that bitcoin will need in the future.

There are two problems with Luria’s argument:

1) As noted above, this does not happen with any other commodity and historically nothing with a perfectly inelastic supply

2) Empirically, as described by Wences Casares above, nearly all the bitcoins held at Xapo (and likely other “hosted wallets”) are being held as investments. This reduces liquidity which translates into volatility due to once again the inability to slowly adjust the supply relative to the shifts in demand. This ties into a number of issues discussed in, What is the “real price” of bitcoin? that are worth revisiting.

Also on page 111, they write that “the exchange rate itself doesn’t matter.”

Actually it does. It directly impacts two things:

1) outside perception on the health of Bitcoin and therefore investor interest (just talk to Buttercoin);

2) on a ten-minute basis it impacts the bottom line of miners. If prices decline, so to is the incentive to generate proof-of-work. Bankruptcy, as CoinTerra faces, is a real phenomenon and if prices decline very quickly then the security of the network can also be reduced due to less proof-of-work being generated

Continuing on page 111:

It’s expected that the mirror version of this will in time be set up for consumers to convert their dollars into bitcoins, which will then immediately be sent to the merchant. Eventually, we could all be blind to these bitcoin conversions happening in the middle of all our transactions.

It’s unfortunate that they do not explain how this will be done without a trusted third party, or why this process is needed. What is the advantage of going from USD-> paying a conversion fee -> BTC -> conversion fee -> back into USD? Why not just spend USD and cut out the Bitcoin middleman?

Lastly on page 111:

Still, someone will have to absorb the exchange-rate risk, if not the payment processors, then the investors with which they trade.

The problem with this is that its generally not in the mandate or scope of most VC firms to purchase commodities or currencies directly. In fact, they may even need some kind of license to do so depending on the jurisdiction (because it is a foreign exchange play). Yet expecting the payment processors to shoulder the volatility is probably a losing proposition: in the event of a protracted bear market how many bitcoins at BitPay — underwater or not — will need to be liquidated to pay for operating costs?4

On page 112 they write:

‘Bitcoin has features from all of them, but none in entirety. So, while it might seem unsatisfying, our best answer to the question of whether cryptocurrency can challenge the Visa and MasterCard duopoly is, “maybe, maybe not.”

On the face of it, it is a safe answer. But upon deeper inspection we can probably say, maybe not. Why? Because for Bitcoin, once again, there is no native method for issuing credit (which is what Visa/MasterCard do with what are essentially micro-loans).

For example, in order to natively add some kind of lending facility within the Bitcoin network a new “identity” system would need to be built and integrated (to enable credit checks) — yet by including real-world “identity” it would remove the pseudonymity of Bitcoin while simultaneously maintaining the same costly proof-of-work Sybil protection. This is again, an unnecessary cost structure entirely and positions Bitcoin as a jack-of-all-trades-but-master-of-none. Why? Again recall that the cost structure is built around Dynamic Membership Multi-Party Signature (DMMS); if the signing validators are static and known you might as well use a database or permissioned ledgers.

Or as Robert Sams recently explained, if censorship resistance is co-opted then the reason for proof-of-work falls to the wayside:

Now, I am sure that the advocates of putting property titles on the bitcoin blockchain will object at this point. They will say that through meta protocols and multi-key signatures, third party authentication of transaction parties can be built-in, and we can create a registered asset system on top of bitcoin. This is true. But what’s the point of doing it that way? In one fell swoop a setup like that completely nullifies the censorship resistance offered by the bitcoin protocol, which is the whole raison d’etre of proof-of-work in the first place! These designs create a centralised transaction censoring system that imports the enormous costs of a decentralised one built for censorship-resistance, the worst of both worlds.

If you are prepared to use trusted third parties for authentication of the counterparts to a transaction, I can see no compelling reason for not also requiring identity authentication of the transaction validators as well. By doing that, you can ditch the gross inefficiencies of proof-of-work and use a consensus algorithm of the one-node-one-vote variety instead that is not only thousands of times more efficient, but also places a governance structure over the validators that is far more resistant to attackers than proof-of-work can ever be.

On page 113, they write:

“the government might be able to take money out of your local bank account, but it couldn’t touch your bitcoin. The Cyprus crisis sparked a stampede of money into bitcoin, which was now seen as a safe haven from the generalized threat of government confiscation everywhere.”

In theory this may be true, but in practice, it is likely that a significant minority — if not majority — of bitcoins are now held in custody at depository institutions such as Xapo, Coinbase and Circle. And these are not off-limits to social engineering. For instance, last week an international joint-task force confiscated $80,000 in bitcoins from dark web operators. The largest known seizure in history were 144,000 bitcoins from Ross Ulbricht (Dread Pirate Roberts) laptop.

Similarly, while it probably is beyond the scope of their book, it would have been interesting to see a survey from Casey and Vigna covering the speculators during this early 2013 time frame. Were the majority of people buying bitcoins during the “Cyprus event” actually worried about confiscation or is this just something that is assumed? Fun fact: the largest transaction to BitPay of all time was on March 25, 2013 during the Cyprus event, amounting to 28,790 bitcoins.

On page 114, the writers for the first time (unless I missed it elsewhere), use the term “virtual currency.” Actually, they quote FinCEN director Jennifer Calvery who says that FincCEN, “recognizes the innovation virtual currencies provide , and the benefits they might offer society.”

Again recall that most fiat currencies today are already digitized in some format — and they are legal tender. In contrast, cryptocurrencies such as bitcoin are not legal tender and are thus more accurately classified as virtual currencies. Perhaps that will change in the future.

On page 118 they note that, “More and more people opened wallets (more than 5 million as of this writing).”

I will get to this later. Note that on p. 123 they say Coupa Cafe has a “digital wallet” a term used throughout the entire book.

Chapter 5

On page 124:

“Bitcoins exist only insofar as they assign value to a bitcoin address, a mini, one-off account with which people and firms send and receive the currency to and from other people’s firms’ addresses.”

This is actually a pretty concise description of best-practices. In reality however, many individuals and organizations (such as exchanges and payment processors) reuse addresses.

Continuing on page 124:

“This is an important distinction because it means there’s no actual currency file or document that can be copied or lost.”

This is untrue. In terms of security, the hardest and most expensive part in practice is securing the credentials — the private key that controls the UTXOs. As Stefan Thomas, Jason Whelan (p. 139) and countless other people on /r/sorryforyourloss have discovered, this can be permanently lost. Bearer assets are a pain to secure, hence the re-sprouting of trusted third parties in Bitcoinland.

One small nitpick in the note at the bottom of page 125, “Sometimes the structure of the bitcoin address network is such that the wallet often can’t send the right amount in one go…” — note that this ‘change‘ is intentional (and very inconvenient to the average user).

Another nitpick on page 128:

Each mining node or computer gathers this information and reduces it into an encrypted alphanumeric string of characters known as a hash.

There is actually no encryption used in Bitcoin, rather there are some cryptographic primitives that are used such as key signing but this is not technically called encryption (the two are different).

On page 130, I thought it was good that they explained where the term nonce was first used — from Lewis Carroll who created the word “frabjous” and described it as a nonce word.

On page 132, in describing proof-of-work:

While that seems like a mammoth task, these are high-powered computers; it’s not nearly as taxing as the nonce-creating game and can be done relatively quickly and easily.

They are correct in that something as simple as a Pi computer can and is used as the actual transaction validating machine. Yet, at one point in 2009, this bifurcation did not exist: a full-node was both a miner and a hasher. Today that is not the case and we technically have about a dozen or so actual miners on the network, the rest of the machines in “farms” just hash midstates.

On page 132, regarding payment processors accepting zero-confirmation transactions:

They do this because non-confirmations — or the double-spending actions that lead to them — are very rare.

True they are very rare today in part because there are very few incentives to actually try and double-spend. Perhaps that will change in the future with new incentives to say, double-spend watermarked coins from NASDAQ.

And if payment processors are accepting zero confirmations, why bother using proof-of-work and confirmations at all? Just because a UTXO is broadcast does not mean it will not be double-spent let alone confirmed and packaged into a block. See also replace-by-fee proposal.

Small note on page 132:

“the bitcoin protocol won’t let it use those bitcoins in a payment until a total of ninety-nine additional blocks have been built on top its block.”

Sometimes it depends on the client and may be up to 120 blocks altogether, not just 100.

On page 133 they write:

“Anyone can become a miner and is free to use whatever computing equipment he or she can come up with to participate.”

This may have been the case in 2009 but not true today. In order to reduce payout variance, the means of production as it were, have gravitated towards large pools of capital in the form of hashing farms. See also: The Gambler’s Guide to Bitcoin Mining.

On page 135 they write:

“Some cryptocurrency designers have created nonprofit foundations and charged them with distributing the coins based on certain criteria — to eligible charities, for example. But that requires the involvement of an identifiable and trusted founder to create the foundation.”

The FinCEN enforcement action and fine on Ripple Labs could put a kibosh on this in the future. Why? If organizations that hand out or sell coins are deemed under the purview of the Bank Secrecy Act (BSA) it is clear that most, if not all, crowdfunding or initial coin offerings (ICO) are violating this by not implementing KYC/AML requirements on participants or filing SARs.

On page 136 they write:

“Both seigniorage and transaction fees represent a transfer of value to those running the network. Still, in the grand scheme of things, these costs are far lower than anything found in the old system.”

This is untrue and an inaccurate comparison. We know that at the current bitcoin price of $240 it costs roughly $315 million to operate the network for the entire year. If bitcoin-based consumer spending patterns hold up and reflect last years trends seen by BitPay, then roughly $350 million will be spent through payment processors, nearly half of which includes mining payouts.

Or in other words, for roughly every dollar spent on commerce another dollar is spent securing it. This is massive oversecurity relative to the commerce involve. Neither Saudi Arabia or even North Korea spend half of, let alone 100% of their GDP on military expenditures (yet).

Chapter 6

Small nitpick on page 140, Butterfly Labs is based in Leawood, Kansas not Missouri (Leawood is on the west side of the dividing line).

I think the story of Jason Whelan is illuminating and could help serve as a warning guide to anyone wanting to splurge on mining hardware.

For instance on page 141:

“And right from the start Whelan face the mathematical reality that his static hashrate was shrinking as a proportion of the ever-expanding network, whose computing power was by then almost doubling every month.”

Not only was this well-written but it does summarize the problem most new miners have when they plan out their capital expenditures. It is impossible to know what the network difficulty will be in 3 months yet what is known is that even if you are willing to tweak the hardware and risk burning out some part of your board, your hashrate could be diluted by faster more efficient machines. And Whelan found out the hard way that he might as well bought and held onto bitcoins than mine. In fact, Whelan did just about everything the wrong way, including buying hashing contracts with cloud miners from “PBCMining.com” (a non-functioning url).

On page 144 the authors discussed the mining farms managed by now-defunct CoinTerra:

With three in-built high-powered fans running at top speed to cool the rig while its internal chi races through calculations, each unit consumes two kilowatts per hour, enough power to run an ordinary laptop for a month. That makes for 20 kWh per tower, about ten times the electricity used for the same space by the neighboring server of more orthodox e-commerce firms.

As noted in Chapter 2 above, this electricity has to be “wasted.” Bitcoin was designed to be “inefficient” otherwise it would be easy to attack and censor. And in the future, it cannot become more “efficient” — there is no free lunch when it comes to protecting it. It also bears mentioning that CoinTerra was sued by its utility company in part for the $12,000 a day in electrical costs that were not being paid for.

On page 145 they wrote that as of June 2014:

“By that time, the network, which was then producing 88,000 trillion hashes every second, had a computing power six thousand times the combined power of the world’s top five hundred supercomputers.”

This is not a fair comparison. ASIC miners can do one sole function, they are unable to do anything aside from reorganize a few fields (such as date and nonce) with the aim of generating a new number below a target number. They cannot run MS Office, Mozilla Firefox and more sobering: they cannot even run a Bitcoin client (the Pi computer run by the pool runs the client).

In contrast, in order to be recognized as a Top 500 computer, only general purpose machines capable of running LINXPACK are considered eligible. The entire comparison is apples-to-oranges.

On page 147 the authors described a study from Guy Lane who used inaccurate energy consumption data from Blockchain.info.

And then they noted that:

“So although the total consumption is significantly higher than the seven-thousand-home estimate, we’re a long way from bitcoin’s adding an entire country’s worth of power consumption to the world.”

This is not quite true. As noted above in the notes of Chapter 2 above, based on Dave Hudson’s calculations the current Bitcoin network consumes the equivalent of about 10% of Ireland’s annual energy usage yet produces two orders of magnitude less economic activity. If the price of bitcoin increases so to does the amount of energy miners are willing to expend to chase after the seigniorage. See also Appendix B.

On page 148 they write that:

For one, power consumption must be measured against the value of validating transactions in a payment system, a social service that gold mining has never provided. Second, the costs must be weighed against the high energy costs of the alternative, traditional payment system, with its bank branches, armored cars, and security systems. And finally, there’s the overriding incentive for efficiency that the profit motive delivers to innovators, which is why we’ve seen such giant reductions in power consumption for the new mining machines. If power costs make mining unprofitable, it will stop.

First of all, validation is cheap and easy, as noted above it is typically done with something like a Pi computer. Second, they could have looked into how much real commerce is taking place on the chain relative to the costs of securing it so the “social service” argument probably falls flat at this time.

Thirdly, the above “armored cars and security systems” is not an apples-to-apples comparison. Bitcoin does not provide any banking service beyond a lock box, it does not provide for home mortgages, small business loans or mezzanine financing. The costs for maintaining those services in the traditional world do not equate to MC=MV as described at the end of Chapter 1 notes.

Fourthly, they ignore the Red Queen effect. If a new hashing machine is invented and consumes half as much energy as before then the farm owner will just double the amount of machines and the net effect is the same as before. This happens in practice, not just in theory, hence the reason why electrical consumption has gone up in aggregate and not down.

On page 149 they write:

“But the genius of the consensus-building in the bitcoin system means such forks shouldn’t be allowed to go on for long. That’s because the mining community works on the assumption that the longest chain is the one that constitutes consensus.”

That’s not quite accurate. Each miner has different incentives. And, as shown empirically with other altcoins, forks can reoccur frequently without incentives that align. For now, some incentives apparently do. But that does not mean that in the future, if say watermarked coins become more common place, that there will not be more frequent forks as certain miners attempt to double-spend or censor such metacoins.

Ironically on page 151 the authors describe the fork situation of March 2013 and describe the fix in which a few core developers convince Mark Karpeles (who ran Mt. Gox) to unilaterally adopt one specific fork. This is not trustless.

On page 151 they write:

“That’s come to be known as a 51 percent attack. Nakamoto’s original paper stated that the bitcoin mining network could be guaranteed to treat everyone’s transactions fairly and honestly so long as no single miner or mining group owned more than 50 percent of the hashing power.”

And continuing on page 153:

“So, the open-source development community is now looking for added protections against selfish mining and 51 percent attacks.”

While they do a good job explaining the issue, they don’t really discuss how it is resolved. And it cannot be without gatekeepers or trusted hardware.

For instance, three weeks ago there was a good reddit thread discussing one of the problems of Andreas Antonopolous’ slippery slope view that you could just kick the attackers off the network. First, there is no quick method for doing so; second, by blacklisting them you introduce a new problem of having the ability to censor miners which would be self-defeating for such a network as it introduces a form of trust into an expensive cost structure of trust minimization.

On page 152 they cite a Coinometrics number:

“in the summer of 2014 the cost of the mining equipment and electricity required for a 51 percent attack stood at $913 million.”

This is a measurement of maximum costs based on hashrate brute force — a Maginot Line attack. In practice it is cheaper to do via out of band attacks (e.g., rubber hose cryptanalysis). There are many other, cheaper ways, to attack the P2P network itself (such as Eclipse attacks).

On page 154 when discussing wealth disparity in Bitcoin they write:

“First, some perspective. As a wealth-gap measure, this is a lousy one. For one, addresses are not wallets. The total number of wallets cannot be known, but they are by definition considerably fewer than the address tally, even though many people hold more than one.”

Finally. So the past several chapters I have mentioned I will discuss wallets at some length. Again, the authors for some reason uncritically cite the “wallet numbers” from Blockchain.info, Coinbase and others as actual digital wallets.

Yet here they explain that these metrics are bupkis. And they are. It costs nothing to generate a wallet and there are scripts you can run to auto generate them. In fact, Zipzap and many others used to give every new user a Blockchain.info wallet por gratis.

And this is problematic because press releases from Xapo and Blockchain.info continually cite a number that is wholly inaccurate and distorting.

For instance Wences Casares said in a presentation a couple months ago that there were 7 million users. Where did that number come from? Are these on-chain privkey holders? Why are journalists not questioning these claims? See also: A brief history of Bitcoin “wallet” growth.

On page 154 they write:

“These elites have an outsize impact on the bitcoin economy. They have a great interest in seeing the currency succeed and are both willing and able to make payments that others might not, simply to encourage adoption.”

Perhaps this is true, but until there is a systematic study of the conspicuous consumption that takes place, it could also be the case that some of these same individuals just have an interest in seeing the price of bitcoin rise and not necessarily be widely adopted. The two are not mutually exclusive.

On page 155 and 156 they describe the bitsat project, to launch a full node into space which is aimed “at making the mining network less concentrated.”

Unfortunately these types of full nodes are not block makers. Thus they do not actually make the network less concentrated, but only add more propagating nodes. The two are not the same.

On page 156 they describe some of the altcoin projects:

“They claim to take the good aspects of bitcoin’s decentralized structure but to get ride of its negative elements, such as the hashing-power arms race, the excessive use of electricity, and the concentration of industrialized mining power.”

I am well aware of the dozens various coin projects out there due to work with a digital asset exchange over the past year. Yet fundamentally all of the proof-of-work based coins end up along the same trend line, if they become popular and reach a certain level of “market cap” (an inaccurate term) specialized chips are designed to hash it.

And the term “excessive” energy related to proof-of-work is a bit of a non-starter. Ignoring proof-of-stake systems, if it becomes less energy intensive to hash via POW, then it also becomes cheaper to attack. Either miners will add more equipment or the price has dropped for the asset and it is therefore cheaper to attack.

On page 157 regarding Litecoin they write that:

“Miners still have an incentive to chase coin rewards, but the arms race and the electricity usage aren’t as intense.”

That’s untrue. Scrypt (which is used instead of Hashcash) is just as energy intensive. Miners will deploy and utilize energy in the same patterns, directly in proportion to the token price. The difference is memory usage (Litecoin was designed to be more memory intensive) but that is unrelated to electrical consumption.

Continuing:

“Litecoin’s main weakness is the corollary of its strength: because it’s cheaper to mine litecoins and because scrypt-based rigs can be used to mine other scrypt-based altcoins such as dogecoin, miners are less heavily invested in permanently working its blockchain.”

This is untrue. Again, Litecoin miners will in general only mine up to the point where it costs a litecoin to make a litecoin. Obviously there are exceptions to it, but in percentage terms the energy usage is the same.

Continuing:

“Some also worry that scrypt-based mining is more insecure, with a less rigorous proof of work, in theory allowing false transactions to get through with incorrect confirmations.”

This is not true. The two difference in security are the difficulty rating and block intervals. The higher the difficulty rating, the more energy is being used to bury blocks and in theory, the more secure the blocks are from reversal.

The question is then, is 2.5 minutes of proof-of-work as secure as burying blocks every 10 minutes? Jonathan Levin, among others, has written about this before.

Small nitpick on page 157, fairly certain that nextcoin should be referred to as NXT.

Small nitpick on page 157, fairly certain that nextcoin should be referred to as NXT.

On page 158 they write:

If bitcoin is to scale up, it must be upgraded sot hat nodes, currently limited to one megabyte of data per ten-minute block, are free to process a much larger set of information. That’s not technically difficult; but it would require miners to hash much larger blocks of transactions without big improvements in their compensation. Developers are currently exploring a transaction-fee model that would provide fairer compensation for miners if the amount of data becomes excessive.

This is not quite right. There is a difference between block makers (pools) and hashers (mining farms). The costs for larger blocks would impact block makers not hashers, as they would need to upgrade their network facilities and local hard drive. This may seem trivial and unimportant, but Jonathan Levin’s research, as well as others suggest that block sizes does in fact impact orphan rates.5

It also impacts the amount of decentralization within the network as larger blocks become more expensive to propagate you will likely have fewer nodes. This has been the topic of immense debate over the past several weeks on social media.

Also on page 158 they write:

The laboratory used by cryptocurrency developers, by contrast, is potentially as big as the world itself, the breadth of humanity that their projects seek to encompass. No company rulebook or top-down set of managerial instructions keeps people’s choice in line with a common corporate objective. Guiding people to optimal behavior in cryptocurrencies is entirely up to how the software is designed to affect human thinking, how effectively its incentive systems encourage that desired behavior

This is wishful thinking and probably unrealistic considering that Bitcoin development permanently suffers from the tragedy of the commons. There is no CEO which is both good and bad.

For example, directions for where development goes is largely based on two things:

- how many upvotes your comment has on reddit (or how many retweets it gets on Twitter)

- your status is largely a function of how many times Satoshi Nakamoto responded to you in email or on the Bitcointalk forum creating a permanent clique of “early adopters” whose opinions are the only valid ones (see False narratives)

This is no way to build a financial product. Yet this type of lobbying is effectively how the community believes it will usurp well-capitalized private entities in the payments space.

Several months ago a user, BitttBurger, made a similar observation:

I’ve said it before and I will say it again. There is a reason why Developers should not be in control of product development priorities, naming, feature lists, or planning for a product. That is the job of the sales, marketing, and product development teams who actually interface with the customer. They are the ones who do the research and know what’s needed for a product. They are the ones who are supposed to decide what things are called, what features come next, and how quickly shit gets out the door.

Bitcoin has none of that. You’ve got a Financial product, being created for a financial market, by a bunch of developers with no experience in finance, and (more importantly) absolutely no way for the market to have any input or control over what gets done, or what it’s called. That is crazy to me.

Luke is a perfect example of why you don’t give developers control over anything other than the structure of the code.

They are not supposed to be making product development decisions. They are not supposed to be naming anything. And they definitely are not supposed to be deciding “what comes next” or how quickly things get done. In any other company, this process would be considered suicide.

Yet for some reason this is considered to be a feature rather than a bug (e.g., “what is your Web of Trust (WoT) number?”).

On page 159 they write:

“The vital thing to remember is that the collective brainpower applied to all the challenges facing bitcoin and other cryptocurrencies is enormous. Under the open-source, decentralized model, these technologies are not hindered by the same constraints that bureaucracies and stodgy corporations face.”

So, what is the Terms of Service for Bitcoin? What is the customer support line? There isn’t one. Caveat emptor is pretty much the marketing slogan and that is perfectly fine for some participants yet expecting global adoption without a “stodgy” “bureaucracy” that helps coordinate customer service seems a bit of a stretch.

And just because there is some avid interest from a number of skilled programmers around the world does not mean public goods problems surrounding development will be resolved.

For reference: there were over 5000 co-authors on a recent physics paper but that doesn’t mean their collective brain power will quickly resolve all the open questions and unsolved problems in physics.

Chapter 7:

Small nitpick on page 160:

“Bitcoin was born out of a crypto-anarchist vision of a decentralized government-free society, a sort of encrypted, networked utopia.”

As noted above, there is actually no encryption used in Bitcoin.

On page 162 they write:

“Before we get too carried away, understand this is still early days.”

That may be the case. Perhaps decentralized cryptocurrencies like Bitcoin are not actually the internet in the early 1990s like many investors claim but rather the internet in the 1980s when there were almost no real use-cases and it is difficult to use. Or 1970s. The problem is no one can actually know the answer ahead of time.

And when you try to get put some milestone down on the ground, the most ardent of enthusiasts move the goal posts — no comparisons with existing tech companies are allowed unless it is to the benefit of Bitcoin somehow. I saw this a lot last summer when I discussed the traction that M-Pesa and Venmo had.

A more recent example is “rebittance” (a portmanteau of “bitcoin” and “remittance”). A couple weeks ago Yakov Kofner, founder of Save On Send, published a really good piece comparing money transmitter operators with bitcoin-related companies noting that there currently is not much meat to the hype. The reaction on reddit was unsurprisingly fist-shaking Bitcoin rules, everyone else drools.

With Yakov Kofner (CEO Save On Send)

When I was in NYC last week I had a chance to meet with him twice. It turns out that he is actually quite interested in Bitcoin and even scoped out a project with a VC-funded Bitcoin company last year for a consumer remittances product.

But they decided not to build and release it for a few reasons:

- in practice, many consumers are not sensitive enough to a few percentage savings because of brand trust/loyalty/habit;

- lacking smartphones and reliable internet infrastructure, the cash-in, cash-out aspect is still the main friction facing most remittance corridors in developing countries, bitcoin does not solve that;

- it boils down to an execution race and it will be hard to compete against incumbents let alone well-funded MTO startups (like TransferWise).

That’s not to say these rebittance products are not good and will not find success in niches.

For instance, I also spoke with Marwan Forzley (below), CEO of Align Commerce last week. Based on our conversation, in terms of volume his B2B product appears to have more traction than BitPay and it’s less than a year old.

What is one of the reasons why? Because the cryptocurrency aspect is fully abstracted away from customers.

Raja Ramachandran (R3CEV), Dan O’Prey (Hyperledger), Daniel Feichtinger (Hyperledger), Marwan Forzley (Align Commerce)

In addition, both BitX and Coins.ph — based on my conversations in Singapore two weeks ago with their teams — seem to be gaining traction in a couple corridors in part because they are focusing on solving actual problems (automating the cash-in/cash-out process) and abstracting away the tech so that the average user is oblivious of what is going on behind the scenes.

Markus Gnirck (StartupBootCamp), Antony Lewis (itBit) and Ron Hose (Coins.ph) at the DBS Hackathon event

On page 162 and 163 the authors write about the Bay Area including 20Mission and Digital Tangible.

There is a joke in this space that every year in cryptoland is accelerated like dog years. While 20Mission, the communal housing venue, still exists, the co-working space shut down late last year. Similarly, Digital Tangible has rebranded as Serica and broadened from just precious metals and into securities. In addition, Dan Held (page 164) left Blockchain.info and is now at ChangeTip.

On page 164 they write:

“But people attending would go on to become big names in the bitcoin world: Among them were Brian Armstrong and Fred Ehrsam, the founders of Coinbase, which is second only to Blockchain as a leader in digital-wallet services and one of the biggest processors of bitcoin payments for businesses.”

10 pages before this they said how useless digital wallet metrics are. It would have been nice to press both Armstrong and Ehrsam to find out what their actual KYC’ed active users to see if the numbers are any different than the dated presentation.

On page 165 they write:

“It’s a very specific type of brain that’s obsessed with bitcoin,” says Adam Draper, the fourth-generation venture capitalist…”

I hear this often but what does that mean? Is investing genetic? If so, surely there are more studies on it?

For instance, later on page 176 they write:

“The youngest Draper, who tells visitors to his personal web site that his life’s ambition is to assist int he creation of an iron-man suit, has clearly inherited his family’s entrepreneurial drive.”

Perhaps Adam Draper is indeed both a bonafide investor and entrepreneur, but it does not seem to be the case that either can be or is necessarily inheritable.

On page 167:

“The only option was to “turn into a fractional-reserve bank,” he said jokingly, referring tot he bank model that allows banks to lend out deposits while holding a fraction of those funds in reserve. “They call it a Ponzi scheme unless you have a banking license.”

Why is this statement not challenged? I am not defending rehypothecation or the current banking model, but fractional reserve banking as it is employed in the US is not a Ponzi scheme.

Also on page 167 they write:

“First, he had trouble with his payments processor, Dwolla which he later sued for $2 million over what Tradehill claimed were undue chargebacks.”

A snarky thing would be to say he should have used bitcoin, no chargebacks. But the issue here, one that the authors should have pressed is that Tradehill, like Coinbase and Xapo, are effectively behaving like banks. It’s unclear why this irony is not discussed once in the book.

For instance, several pages later on page 170 they once again talk about wallets:

The word wallet is thrown around a lot in bitcoin circles, and it’s an evocative description, but it’s just a user application that allows you to send and receive bitcoins over the bitcoin network. You can download software to create your own wallet — if you really want to be your own bank — but most people go through a wallet provider such as Coinbase or Blockchain, which melded them into user-friendly Web sites and smart phone apps.

I am not sure if it is intentional but the authors clearly understand that holding a private key is the equivalent of being a bank. But rather than say Coinbase is a bank (because they too control private keys), they call them a wallet provider. I have no inside track into how regulators view this but the euphemism of “wallet provider” is thin gruel.

On the other hand Blockchain.info does not hold custody of keys but instead provide a user interface — at no point do they touch a privkey (though that does not mean they could not via a man-in-the-middle-attack or scripting errors like the one last December).

On page 171 they talk about Nathan Lands:

The thirty-year-old high school dropout is the cofounder of QuickCoin, the maker of a wallet that’s aimed directly at finding the fastest easiest route to mass adoption. The idea, which he dreamed up with fellow bitcoiner Marshall Hayner one night over a dinner at Ramen Underground, is to give nontechnical bitcoin newcomers access to an easy-to-use mobile wallet viat familiar tools of social media.

Unfortunately this is not how it happened. More in a moment.

Continuing the authors write:

“His successes allowed Lands to raise $10 million for one company, Gamestreamer.”

Actually it was Gamify he raised money for (part of the confusion may be due to how it is phrased on his LinkedIn profile).

Next the authors state:

“He started buying coins online, where her ran into his eventual business partner, Hayner (with whom he later had a falling-out, and whose stake he bought).”

One of the biggest problems I had with this book is that the authors take claims at face value. To be fair, I probably did a bit too much myself with GCON.

On this point, I checked with Marshall Hayner who noted that this narrative was untrue: “Nathan never bought my stake, nor was I notified of any such exchange.”

While the co-founder dispute deserves its own article or two, the rough timeline is that in late 2013 Hayner created QuickCoin and then several months later on brought Lands on to be the CEO. After a soft launch in May 2014 (which my wife and I attended, see below) Lands maneuvered and got the other employees to first reduce the equity that Hayner had and then fired him so they could open up the cap table to other investors.

QuickCoin launch party with Marshall Hayner, Jackson Palmer (Dogecoin), and my wife

With Hayner out, QuickCoin quickly faded due to the fact that the team had no ties to the local cryptocurrency community. Hayner went on to join Stellar and is now the co-founder of Trees. QuickCoin folded by the end of the year and Lands started Blockai.